This week the Senate Banking Committee held a hearing titled Perspectives on Challenges in the Property Insurance Market and the Impact on Consumers, a topic that has gained coverage and industry attention in recent months. The witness panel included experts from the insurance and multifamily housing industries; Douglas Heller, Director of Insurance, Consumer Federation of America; Michelle Norris, Executive Vice President of External Affairs and Strategic Partnerships, National Church Residences; and Jerry Theodorou, Policy Director, Finance, Insurance and Trade, The R Street Institute. The AHTCC provided a statement for the record in response to the hearing that underscores the escalating impact of property insurance premium inflation on affordable rental housing development.

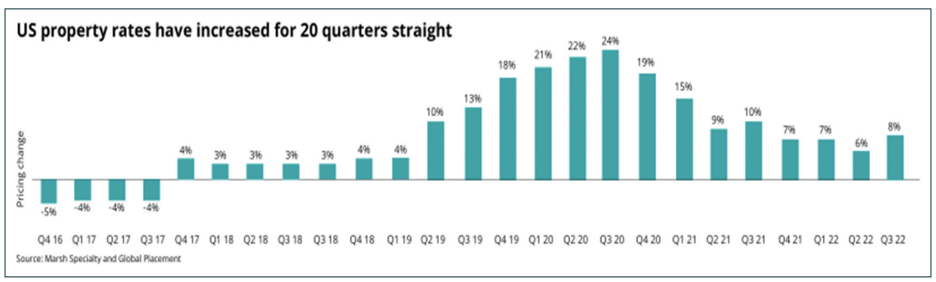

According to a recent survey from the National Multi Housing Council, as of the first quarter of 2023, property insurance rates in the United States have increased for twenty-two consecutive quarters. Over the past three years, insurance premiums have skyrocketed, with many owners having experienced year-over-year premium increases from 30 to 100+ percent at affordable rental housing communities.

During the hearing, committee members addressed challenges insurers face, such as climate change-related disasters and regulatory barriers, and solutions, such as implementing a federal backstop and increasing building resiliency. Chairman Sherrod Brown (D-OH) opened the hearing heavily emphasizing the impact of the increased frequency of natural disasters on access to quality, affordable property insurance. He noted that insurer withdrawals from state markets at times leave homeowners with last-resort state-mandated insurance policies, which come with bare-minimum coverage. In his opening statement, Ranking Member Tim Scott (R-SC) recognized the challenges that insurance companies face when trying to remain viable in certain markets and cited high attorney fees as a driver of rising costs.

Witnesses fielded questions pertaining to the drivers of rising insurance costs, the impact on homeowners, and potential solutions. Michelle Norris of National Church Residences (NCR) raised the impact that rising insurance costs are having on affordable rental housing. She emphasized that the issue impacts the production of new affordable rental housing and the viability of existing properties. Natural disasters in the last year have resulted in NCR’s most expensive insurance claims ever. Multiple carriers walked away from offering policies for some impacted NCR properties and others took a take-it-or-leave-it approach while offering higher rates. Jerry Theodorou of The R Street Institute highlighted that there are differences in insurance challenges between states and mentioned some of the solutions being implemented to address them, such as recent tort reform in Florida. Mr. Theodorou was in agreement with Sen. Scott’s opinion that the federal government should not subsidize state insurance needs and added that a federal backstop would backfire because the insurance market is not failing, but adapting to the current context. Sen. Thom Tillis (R-NC) and Sen. Scott commented that reform belongs at the state level to address state-specific insurance market issues.

The National Flood Insurance Program was frequently raised as an example of the federal government’s current involvement in property insurance. Sen. Bob Menendez (D-NJ) raised his NFIP Reauthorization and Reform Act during discussion regarding the need for increased flood insurance across the nation. Mr. Theodorou affirms that the private market is starting to increase flood insurance policies after largely excluding it from homeowner policies since the 1970s – there are now 77 companies writing flood insurance policies. Douglas Heller said we need a federal backstop reinsurance to enable us to push flood insurance back out to the private market. He says that Americans are underinsured for flood events. Additionally, incorporating means testing into the insurance process was briefly discussed and seemed to have the support of Democrats and Republicans.

At the direction of the President, the Federal Insurance Office (FIO) in the Treasury has proposed collecting additional data from insurers on the impact of climate change on the insurance markets to proactively protect consumers. Sen. Elizabeth Warren (D-MA) questioned if this would be helpful in protecting consumers, and Mr. Heller affirmed that it would be helpful and there is a need for it to understand and assess risk. It appears to Sen. Warren that state regulators are opposed to collecting this data and implementing climate risk mitigation strategies.

The challenges facing insurers are impacting their financial viability in certain markets. Some insurers are paying out more in claims than they are taking in from premiums, and this is where the reinsurers come in to cover the loss. Sen. Cortez Masto (D-NV) underscored the impact these issues have on affordable housing, asking Ms. Norris to expand on how rising insurance costs can push affordable housing providers out of the affordable housing market. Ms. Norris shared two basic principles of affordable housing; rent to those who cannot afford market-rate rent and do not charge them more than they can afford. She explained how affordable housing providers cannot simply raise rents when insurance premiums go up, leaving providers in a situation where expenses can crush operational margin – or even their ability to cover costs. This jeopardizes the operation of existing affordable housing developments and the production of affordable housing. Mr. Heller added that non-profits have trouble in property insurance markets, and Sen. Brown’s efforts to have risk retention programs available to non-profits would be helpful. Mr. Heller also mentioned the impact of underwriting guidelines that consider zip code and other potentially discriminating factors as a driver of lacking access to affordable insurance for affordable rental housing.

This coverage of the Senate Banking Committee hearing is part of the AHTCC insurance working group’s efforts to shed light on rising insurance costs and help address its impact on affordable housing production. If you are interested in learning more about the AHTCC’s working group to explore potential policy responses, please email Selia Koss at selia.koss@taxcreditcoalition.org.

Comments are closed.